The iGaming Oligopoly: How Regulation and Costs Triggered a Multi-Billion Dollar Consolidation Wave

The global iGaming industry is undergoing an unprecedented structural transformation.

The era of the digital 'Wild West' - a fragmented landscape of hundreds of independent game studios, niche software providers, and regional operators - is drawing to a decisive close.

In its place, a mature, highly institutionalised corporate structure is taking shape - one in which access to capital and regulatory scale, not creative agility, dictate survival.

Over the past three years, a relentless wave of mergers and acquisitions (M&A) has swept the sector. This consolidation is not opportunistic empire-building; it is a defensive imperative.

Escalating compliance costs, a global pivot toward strict local licensing, and structural margin compression are pushing the industry toward an unmistakably oligopolistic structure, dominated by a handful of multi-billion dollar conglomerates.

The regulatory catalyst: an industry-wide margin squeeze

To understand why the world's largest gambling enterprises are committing billions to acquisitions, one must begin with the regulatory environment.

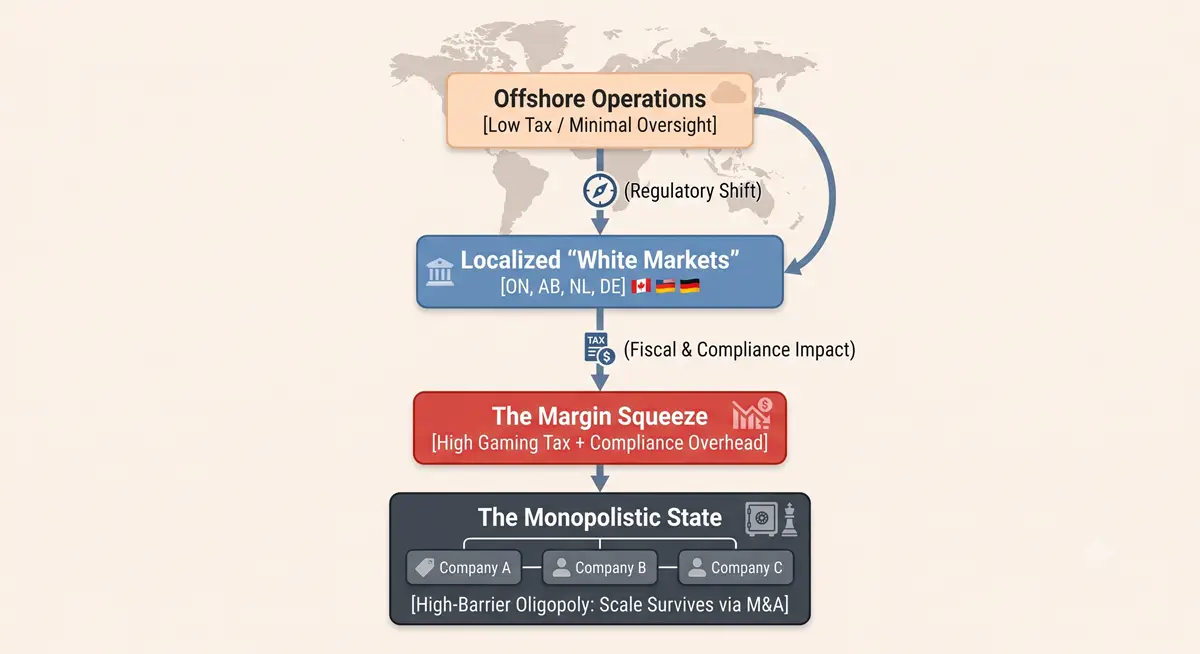

Historically, operators serviced vast international markets from low-tax offshore jurisdictions. That model is now commercially unsustainable.

Sovereign states and federal provinces are systematically dismantling gray markets in favour of strict, localised "white market" regimes - each demanding dedicated licensing, geolocation infrastructure, and localised tax remittance.

Europe as the blueprint

Europe established the template. The Netherlands (via the Remote Gambling Act) and Germany (via the Interstate Treaty on Gambling) built tightly controlled frameworks that legitimise mainstream operation.

Yet they impose hard caps on marketing, mandatory responsible-gambling contributions, and heavy fiscal burdens.

The UK's 2026 enforcement escalations and stricter affordability compliance timelines have intensified this trend. The net effect across Europe is a persistent drag on EBITDA that only scaled operators can absorb.

The Canadian axis: Ontario's proof of concept and Alberta's opening

This regulatory tide has now firmly reached North America, and the numbers validate the model. Ontario pioneered the shift, opening a fully regulated, competitive iGaming market in April 2022.

In 2025 the province handled a staggering $98.3 billion CAD in total wagers, generating roughly $4 billion CAD in Gross Gaming Revenue (GGR). At a 20% tax rate, that yielded some $807 million CAD in provincial tax revenue in a single year.

The growth trajectory has shown no signs of slowing. Through just the first quarter of 2026, Ontarians wagered $27.8 billion CAD on licensed sites, with operators collecting $1.13 billion CAD in revenue.

It is a fiscal outcome no neighbouring treasury can ignore, as our coverage of Ontario's record iGaming market details.

Western Canada's expansion was officially laid by Bill 48 (the iGaming Alberta Act) in 2025. Following updates to the Gaming, Liquor and Cannabis Regulation (GLCR) in January 2026, Alberta is legally scheduled to open its competitive, multi-operator marketplace on July 13, 2026.

That formally ends the monopoly long held by the state-run PlayAlberta platform. We examine it in why Alberta could become Canada's next major online gambling market.

The transmission mechanism of capital

The financial transmission mechanism here is straightforward. Offshore operations built for low tax and minimal oversight are being compressed into strict, localised frameworks.

For small to mid-sized operators, the CapEx required to secure regional licences, integrate localised geolocation tech, and stand up FINTRAC-compliant Know Your Customer (KYC) and Anti-Money Laundering (AML) infrastructures is prohibitive.

This capital must be committed before a single dollar of revenue is generated. When fixed compliance costs outrun regional player yields, the environment becomes unviable for sub-scale firms.

The result is a high-barrier-to-entry oligopoly in which scale is the only durable shield for profitability - and the primary engine of the consolidation wave.

M&A trend I: B2C megadeals and the purchase of market access

Confronted by these high barriers to entry, the sector's absolute giants have turned to mega-acquisitions as their principal vehicle for international expansion.

Rather than incurring the cost and execution risk of building a brand organically in a newly regulated country, market leaders deploy massive cash reserves to buy existing, licensed market share outright.

No corporation has pursued this strategy more aggressively than Flutter Entertainment Plc. In April 2025 it completed its monumental €2.3 billion ($2.6 billion USD) all-cash acquisition of Italian gaming leader Snaitech S.p.A. from Playtech.

The deal was struck at roughly a 9x EBITDA multiple against Snaitech's ~€256 million EBITDA, with Flutter guiding to some €70 million in annualised cost synergies within three years.

It instantly established Flutter as the dominant force in Italy's reshaped digital ecosystem. In parallel, Flutter took a $350 million majority stake in the NSX Group - parent of Betnacional - securing a turnkey position ahead of Brazil's federal iGaming rollout.

The consolidation pattern extends across every tier of the consumer-facing sector.

Evoke plc (formerly 888 Holdings): under strain from UK tax regimes and heavy debt restructuring, Evoke became a target for institutional reshaping, ultimately accepting a £243.1 million buyout from Bally's and Intralot in mid-2026.

Banijay Gaming: the European media conglomerate expanded its wagering footprint by acquiring Germany's Tipico Group in early 2026, then absorbing French casino operator JOA to build an omnichannel powerhouse across Western Europe.

M&A trend II: B2B consolidation and vertical integration

While B2C operators consolidate the consumer-facing market, a parallel - and arguably more consequential - wave is reshaping the B2B supply chain. Aggregators and platform infrastructure providers are aggressively absorbing independent slot studios and live-casino developers.

The strategic objective is two-fold: vertical integration to eliminate third-party licensing fees, and the acquisition of exclusive intellectual property (IP) to differentiate platforms in an increasingly homogenised digital landscape.

| Acquiring entity | Target asset | Deal value / valuation | Strategic objective |

|---|---|---|---|

| EveryMatrix | Fantasma Games AB (Sweden) | SEK 209.8M (~$20.2M USD); SEK 59/share, a 21.4% premium | Vertical content integration - internalises a studio with a 36% EBITDA margin to supply exclusive IP directly to its 250+ operator network, bypassing the margin-diluting middleware layer. |

| Apollo Global Management | IGT Gaming & Digital + Everi Holdings | $6.3B (all-cash) | Private-equity carve-out merging legacy land-based and digital infrastructure into a single private entity - institutional validation of the sector's maturity. |

| Evolution AB | Galaxy Gaming Inc. | Undisclosed (extended to mid-2026) | Secures outright ownership of premium live-dealer table titles and proprietary side-bet mathematics. |

The EveryMatrix-Fantasma transaction crystallises the financial logic of this trend. By acquiring a studio operating at a highly efficient 36% EBITDA margin, the aggregator converts a variable, third-party licensing expense into a high-margin, wholly owned corporate asset.

On an even grander scale, Apollo Global Management's $6.3 billion involvement signals the institutional maturity of iGaming tech. Taking two of the sector's largest infrastructure names private proves core gambling technology is now priced as a stable, cash-generative utility asset class.

The innovation paradox

For market analysts and industry observers, this relentless consolidation wave introduces a complex economic dilemma: the innovation paradox.

As small, independent developers, studios survive purely by taking outsized creative risks - unique mechanics, highly volatile math models, and niche themes designed to stand out in crowded operator lobbies.

Once absorbed by conglomerates like Light & Wonder, Evolution, or EveryMatrix, these creative teams are folded into rigid corporate frameworks optimised for predictable, recurring output.

The structural risk: history suggests corporate consolidation drives product homogenisation. Slot portfolios and live-casino platforms may steadily converge on low-risk, iterative releases engineered to maximise near-term EBITDA optimization rather than category-defining innovation.

Paradoxically, this corporate gridlock creates a definitive opening for a different class of participant. As operators divert capital toward compliance overhead, restructuring, and complex platform migrations, an elite tier of authoritative, pure-play information platforms can capture the consumer narrative.

By delivering transparent, fiercely objective, data-driven market analysis, these independent information engines bridge the widening trust gap for consumers who feel increasingly detached from faceless, multi-billion dollar gambling monopolies.

The corporate terrain of iGaming has shifted permanently. The future belongs not to the swift or the eccentric, but to those with the scale, capital discipline, and institutional regulatory infrastructure to weather a fully globalised white market.

Sources

This article was prepared using official Canadian legal, regulatory and provincial gambling sources, including:

- 1iGaming Ontario (iGO): Annual Market Performance & Fiscal Revenue Reports (2025-2026)

Official iGO reporting underpinning Ontario's figures: $98.3B CAD wagered and ~$807M CAD in 2025 tax revenue, plus $27.8B CAD wagered and $1.13B CAD in operator revenue in Q1 2026.

- 2Alberta Gaming, Liquor and Cannabis (AGLC) - GLCR January 2026 Updates

Bill 48 (the iGaming Alberta Act) and the GLCR regulatory updates confirming the multi-operator market opening on July 13, 2026 and the end of the PlayAlberta monopoly.

- 3Flutter Entertainment Plc: Investor Relations & Definitive Merger Filings (Snaitech & NSX Group)

Investor disclosures on the €2.3B ($2.6B USD) Snaitech acquisition at ~9x EBITDA (€256M EBITDA) with ~€70M targeted synergies, and the $350M NSX Group (Betnacional) majority stake.

- 4EveryMatrix Software Ltd Corporate Newsroom (Fantasma Tender Offer)

Public tender offer for Fantasma Games AB: SEK 209.8M (~$20.2M USD) at SEK 59/share, a 21.4% premium, integrating a studio with a 36% EBITDA margin across 250+ operators.

- 5Apollo Global Management Asset Portal ($6.3bn IGT-Everi Merger)

Apollo's $6.3 billion all-cash private-equity carve-out merging IGT Gaming and Everi Holdings and taking them private.